For most of the last forty years, the forklift fuel question had a simple answer: propane for outdoors and tough duty, electric for indoor warehouses, diesel for the heaviest work. In 2026, that simple answer is wrong often enough that plant managers need to actually run the numbers. Here is what has changed, where each fuel still wins, and the decision framework that resilient warehouse operations are using to plan their fleets through the rest of the decade.

Walk into ten different warehouses in the United States and you will see ten different forklift fleets. Some are entirely propane. Some are entirely electric. Some are running a deliberate mix, with electric trucks indoors and propane out in the yard. A growing number are running lithium-ion electric trucks in operations that would have been considered impossible for electric forklifts five years ago, including three-shift distribution centres, food processing plants, and even some cold storage operations.

The reason for the variation is not that some operators have figured something out and others have not. The reason is that the underlying economics have shifted, the technology on both sides has matured, and the right answer now genuinely depends on the operation. A warehouse running a single shift of light-duty pallet handling is going to make a very different decision from a 24/7 lumberyard or a frozen food distribution centre.

Most plant managers know roughly what the trade-offs are. Propane forklifts cost less upfront, refuel in three minutes, run hard outdoors, and never wait for a charger. Electric forklifts cost more upfront, run cleaner, cost less to operate over time, and dominate enclosed indoor environments. What has changed in the last eighteen months is the size of those advantages, the conditions under which they hold, and the emergence of lithium-ion battery technology that has erased several of the historical limitations on electric forklifts.

This piece walks through what the math actually looks like in 2026, where each fuel still wins, and the procurement and operational decisions that follow from picking the right answer for your specific facility.

The Headline Numbers in 2026

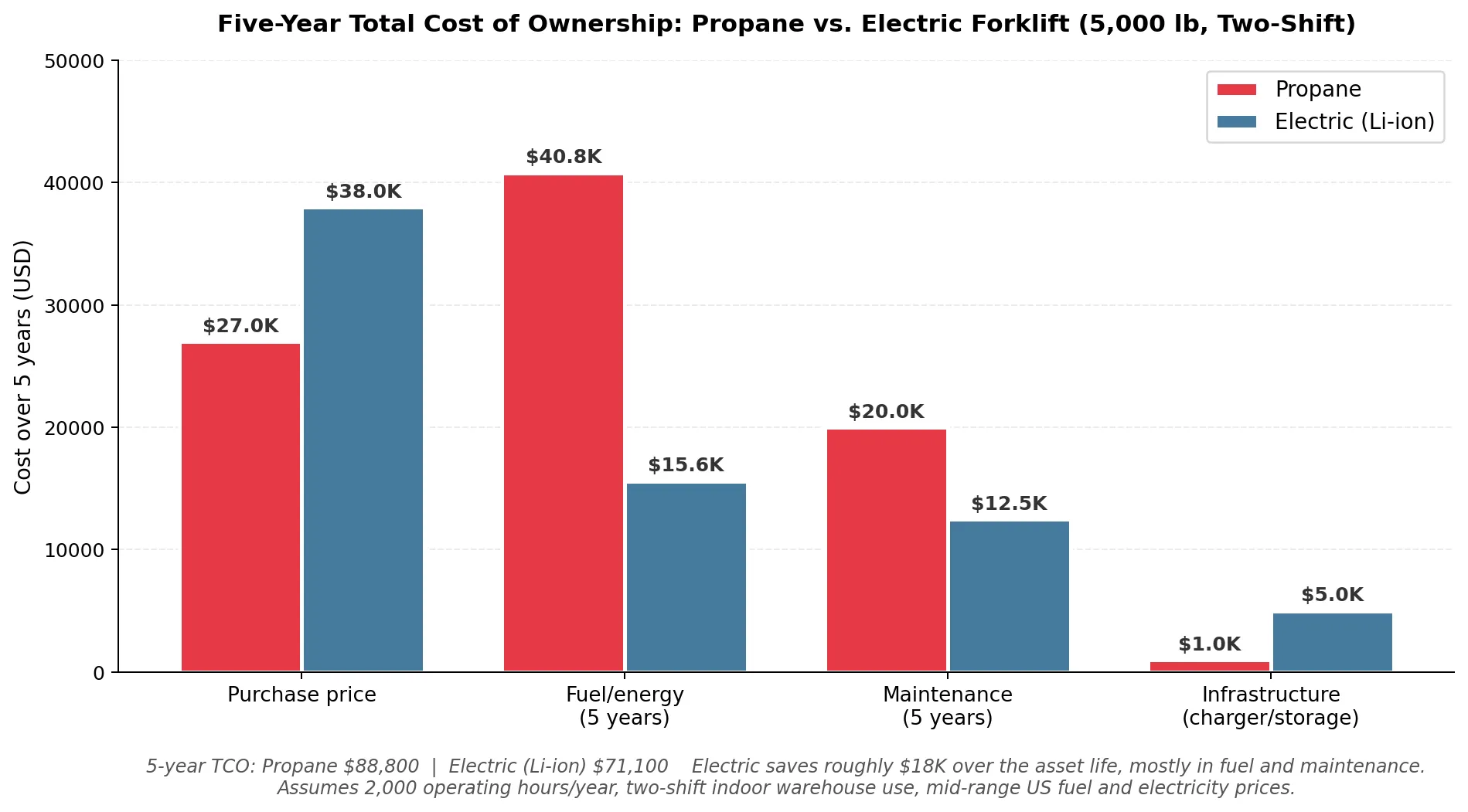

Start with purchase price. A new 5,000-pound capacity cushion-tire propane forklift costs roughly $24,000 to $30,000 in 2026 depending on configuration and options. An equivalent electric forklift, including battery and charger, costs $35,000 to $40,500. That is a $10,000 to $14,000 upfront premium for the electric truck, and it is the single number that has been driving fleet managers toward propane for decades.

Where the math gets interesting is in the operating cost. Industry data from First Energy and from extended operator studies consistently show electric forklifts costing 30 to 75% less to operate per hour than propane equivalents. The numbers break down across three components. Fuel: a propane forklift consumes roughly 1 to 2 gallons of propane per operating hour, which at current Mont Belvieu-influenced US retail propane prices ($2.78 to $4.05 per gallon for forklift cylinder propane in mid-2026) works out to $3 to $8 per hour. An electric forklift consumes 9 to 15 kWh per operating hour, which at average US commercial electricity rates of around $0.13 per kWh works out to roughly $1.20 to $2.00 per hour. Maintenance: propane forklifts cost around $2.00 per operating hour to maintain, primarily due to combustion engine service requirements. Electric forklifts cost around $1.25 per hour, a roughly 40% reduction.

Run those numbers across a typical two-shift indoor warehouse operation (about 2,000 operating hours per year, five years of asset life) and the total cost of ownership picture looks like this.

Across a five-year lifecycle, electric forklifts save roughly $17,700 versus propane for a typical two-shift indoor operation. The savings come almost entirely from lower fuel and maintenance costs, not from the upfront purchase price.

The takeaway is straightforward. For a typical indoor multi-shift warehouse, electric forklifts now deliver meaningfully lower total cost of ownership across the asset life, despite costing more upfront. The break-even point is usually two to three years into operation. After that, every additional hour of operation is saving money compared to the propane alternative.

But that is the average. The right decision for any specific facility depends on a set of operational variables that often push the math in different directions.

Where Electric Has Genuinely Pulled Ahead

Five things have changed in the last few years to make electric forklifts the default choice for a much wider range of operations than they used to be.

First, lithium-ion has replaced lead-acid as the dominant battery chemistry in new electric forklift purchases. Lithium iron phosphate (LiFePO4) batteries last 3,000 or more charge cycles compared to 1,000 to 1,500 for lead-acid, support opportunity charging during operator breaks without damaging battery life, deliver consistent voltage throughout the discharge cycle (rather than slowing down as the battery drains), and eliminate the maintenance overhead of watering, equalisation, and ventilated battery rooms. A single lithium-ion battery can support a forklift through a full multi-shift day without swapping, which is the single most important operational improvement.

Second, opportunity charging has effectively eliminated the downtime argument against electric forklifts. The old rule of thumb that electric trucks need 8 hours to charge and a cooling period before reuse is now a lead-acid artifact. Modern lithium-ion electric forklifts can recover meaningful capacity in 15 to 30 minutes of opportunity charging during operator breaks, and can reach 80% state of charge in under 45 minutes on fast chargers. For most operations, that means the truck is ready to go again whenever the operator is.

Third, the indoor air quality regulatory environment has tightened. OSHA and local insurance inspectors have become more focused on indoor CO and NOx exposure from propane forklifts, particularly in food, pharmaceutical, and beverage facilities. Some operators are now required to install or upgrade ventilation systems to keep running propane indoors, and the cost of those upgrades can exceed the cost of replacing the fleet. In food processing specifically, the Canadian government and several US state agencies now recommend or require electric forklifts in food-contact areas to prevent contamination concerns.

Fourth, cold storage is no longer the propane-only domain it used to be. Lithium-ion batteries with integrated thermal management now maintain over 80% of their capacity at temperatures down to -22°F, which covers most freezer warehouse applications. Lead-acid batteries lose 20 to 40% of their capacity below freezing, which is why cold storage was historically a propane stronghold. That is changing fast.

Fifth, AGV and AMR fleets are almost exclusively lithium-electric. As warehouse automation has expanded, the autonomous mobile robot and automated guided vehicle category has become a meaningful share of new material handling spend, and it is essentially incompatible with propane. Any operation moving toward automation is moving toward electric by default.

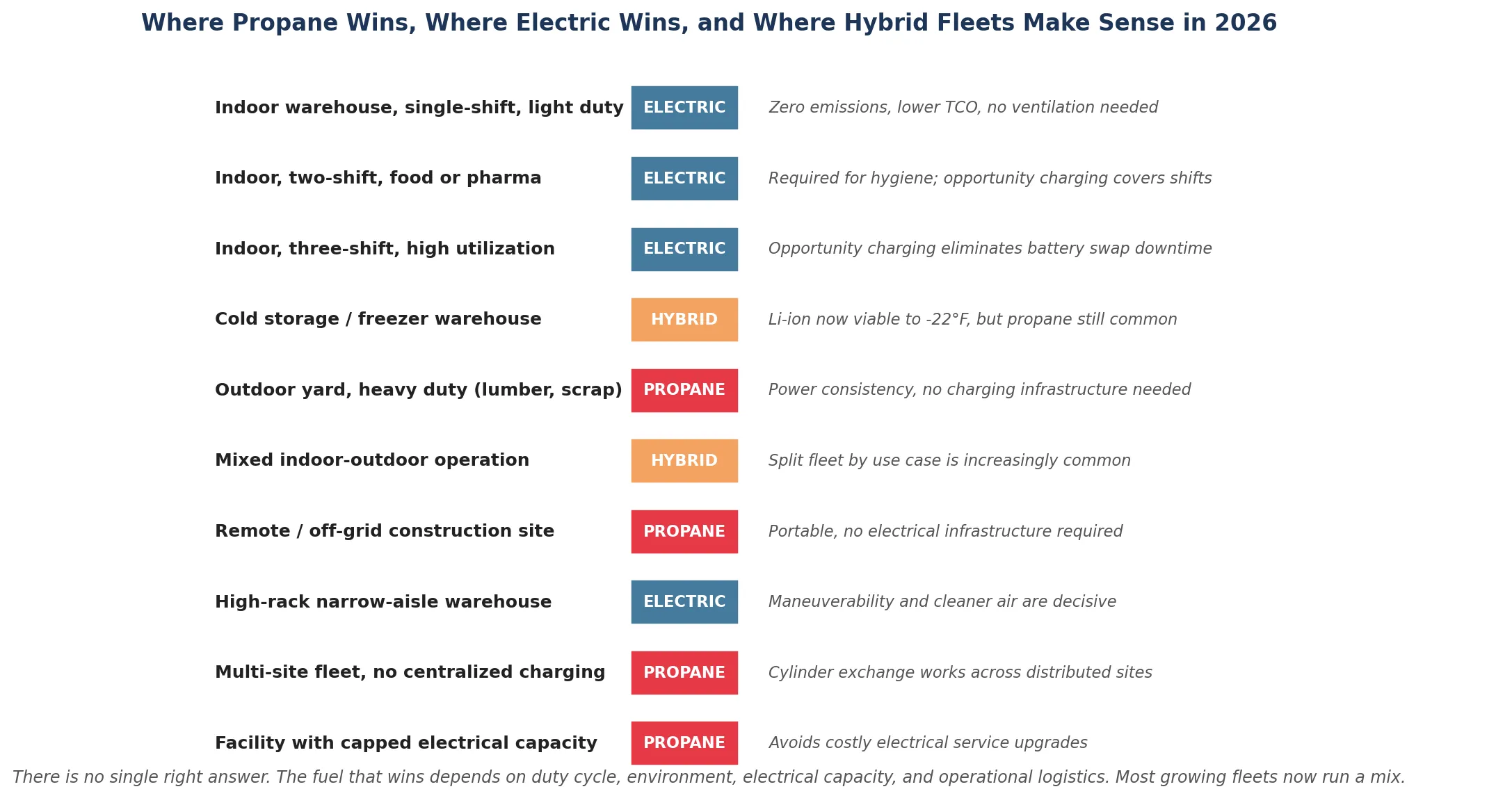

Where Propane Still Wins (And Will Keep Winning)

Despite all of the above, propane forklifts continue to dominate roughly half of the US fleet, and there are good operational reasons for that. The contexts where propane wins are not edge cases. They are large, structurally important categories that the propane forklift industry continues to serve well.

Heavy outdoor operations are the first category. Lumberyards, scrap yards, construction sites, concrete operations, port logistics, and any facility handling oversized or extremely heavy loads in outdoor or semi-outdoor environments are still propane country. The reasons are straightforward. Propane forklifts deliver consistent 100% rated power from start to finish of a shift, while electric trucks (even lithium-ion) can lose 10 to 20% of lifting speed and torque as the battery approaches the lower end of its charge. For operators lifting maximum-rated loads continuously throughout a shift, that performance difference shows up directly in throughput. Propane is also weather-resistant in a way that electric infrastructure is not. A propane forklift in a muddy lumberyard in the rain works exactly the same as a propane forklift in a clean indoor warehouse. An electric forklift in the same environment needs IP-rated waterproofing and careful management of the charging infrastructure.

Facilities with capped or expensive electrical service are the second category. In a lot of older industrial sites, the electrical service was sized for a much smaller operation and upgrading to handle a fleet of electric forklift chargers requires a new transformer, a new electrical panel, and possibly a new utility service connection. For a facility that would otherwise need $50,000 to $200,000 of electrical upgrades to support an electric fleet, propane often wins by default. The same logic applies to facilities in remote areas where utility power is unreliable or expensive.

Multi-site distributed operations are the third category. A company that runs ten small warehouses spread across a region, with no centralised charging infrastructure at any of them, can refuel a propane fleet through a single cylinder exchange service across all locations. Building out electric charging infrastructure at ten separate sites is a significantly larger capital commitment.

Construction sites and temporary operations are the fourth category. Anywhere the operation moves or is short-term, propane has structural advantages. You can drop a propane forklift on a job site and refuel it from cylinders the same day. Setting up electric charging infrastructure for a six-month project rarely pencils out.

Cold storage above the freezing point is the fifth category, though this is the one most actively being eroded. Refrigerated warehouses operating above 32°F (above-freezing coolers for produce, dairy, beverage) are increasingly going electric. Hard-freeze operations (frozen food, ice cream, certain pharmaceutical applications below -10°F) are still mostly propane, even as lithium-ion technology improves. Operators in this segment tend to wait for proven multi-year deployments at peer facilities before switching.

The Hybrid Fleet Has Become the New Default

The most important shift in fleet planning over the last few years has not been propane versus electric. It has been the rise of the deliberately mixed fleet. Operations that used to run a single fuel type across all of their forklifts are increasingly splitting the fleet by use case. Indoor pallet handling and put-away on electric. Outdoor yard work and truck loading on propane. Specialised cold storage on whichever fuel matches the duty cycle.

There are three reasons hybrid fleets have become the default for growing operations.

First, hybrid fleets let operators optimise per-truck rather than fleet-wide. A 30-truck fleet that splits 20 electric (indoor) and 10 propane (outdoor and heavy duty) usually delivers lower total cost than the same fleet run on either fuel exclusively. The savings come from putting each truck on the fuel that matches its actual duty cycle rather than forcing a single fuel to cover use cases it does not fit.

Second, hybrid fleets give operators flexibility during fuel cost spikes. When propane prices spike (typically in winter heating season or when US export demand from Asia surges), the propane portion of the fleet can run lower intensity while the electric portion picks up the work. When electricity rates spike (peak demand charges during hot summers), the reverse plays out. Single-fuel fleets do not have this hedge.

Third, hybrid fleets reduce single-point-of-failure risk. A facility that runs entirely on electric forklifts has a real exposure to grid disruption, transformer failures, or charger downtime. A facility that runs entirely on propane forklifts has exposure to fuel delivery disruptions and cylinder supply tightness. Running both means that one disruption never takes the whole fleet offline.

The right fuel depends on the actual operation. Most growing fleets in 2026 run a deliberate mix, optimising each truck for the duty cycle it actually performs rather than forcing a single fuel across the entire fleet.

The Decision Framework

For plant managers and procurement leads who need to actually make this decision, here is the framework that the most operationally disciplined warehouse operators use.

✓ Map the duty cycle of every truck in the fleet. How many hours per shift, how many shifts, what loads, what environments, indoor or outdoor. This is the single most important data set in the decision.

✓ Run the actual TCO numbers for your facility, not the industry averages. Plug in your local electricity rates (commercial peak demand charges vary widely by region), your actual propane delivered price (cylinder exchange contracts have wildly different all-in costs), and your existing electrical capacity.

✓ Audit your electrical service. If your facility cannot support the additional load of an electric fleet without a service upgrade, factor that capital cost into the comparison. Sometimes it changes the answer.

✓ Check your indoor air quality compliance situation. If you are running propane indoors today and your jurisdiction is tightening ventilation requirements, the cost of compliance may exceed the cost of switching.

✓ Talk to operators at peer facilities who have already made the transition. Real-world experience with two-year-old lithium-ion fleets in conditions similar to yours is worth more than vendor specifications.

✓ Plan for hybrid by default. Unless your operation is unusually homogeneous, the right answer is probably to split the fleet by use case rather than picking a single fuel for everything.

✓ Build supplier relationships on both sides. If you are going to run any propane fleet at all, your propane supplier relationship matters as much as your electric truck supplier relationship. Treat it that way.

The Supply Side: What to Look For in a Propane Distributor

For operations that are keeping propane in their fleet (either fully or as part of a hybrid model), the choice of propane distributor matters significantly more than most operators realise. The propane market in 2026 is more volatile than it has been in years. US propane is now an export-driven commodity, with Mont Belvieu prices responding to Chinese tariff dynamics, Saudi Aramco contract prices, and European demand cycles rather than just US domestic conditions. Inventories sit at record highs in some months and tighten sharply in others. Forklift cylinder supply has become a real operational concern.

The dimensions that separate a strong industrial propane distributor from a weak one have become more important as the underlying market has gotten less stable. Multi-source sourcing across regional terminals, reliable cylinder exchange logistics, predictable pricing contract structures, and emergency service capability are the four operational characteristics that matter most. Regional distributors often outperform national majors on these dimensions, particularly response time and account-level service. Texas-based industrial operations, for example, evaluate distributors such as Southwest Gases, which provides commercial propane cylinder delivery, bulk tank installations, and emergency service across Dallas, Houston, Austin, San Antonio, and Fort Worth, precisely because regional distributors with diversified sourcing and service-level commitments tend to deliver more reliably during the kinds of supply disruptions that have hit the propane market recently. The pattern is consistent across most US regional markets.

Where This Is Going

Three things are worth watching for industrial operations planning fleet investments over the next five years.

The first is the continued maturation of lithium-ion electric forklifts. Battery chemistries are still improving. Charging speeds are still increasing. Cold-weather performance is still expanding. The category of operations where electric is genuinely viable will keep expanding. Operations that decided against electric three years ago should revisit the math today, because the answer has probably changed.

The second is the growing influence of AGV and AMR adoption. Automated material handling is starting to consume a meaningful share of new equipment spend in large distribution and manufacturing operations, and it is almost exclusively electric. Operations that automate are moving toward electric whether or not they were planning to.

The third is the evolving propane market dynamics. US propane production growth has slowed from roughly 10% annually during 2022 to 2024 down to under 5% expected in 2025 and 2026, while export demand from Asia continues to grow. Domestic forklift propane pricing should remain manageable but is going to be more volatile than it has been historically. Operators staying on propane should plan accordingly, with multi-year supply contracts and diversified supplier relationships rather than spot purchases.

The Bottom Line

There is no single right answer to the forklift fuel question in 2026. There is only the right answer for your specific facility, your specific duty cycles, your specific electrical infrastructure, and your specific operational priorities.

What has changed is that the analysis is no longer something you can default-answer based on what you bought ten years ago. Electric has gotten genuinely better, faster, and more flexible. Propane is still the right answer for a meaningful share of industrial use cases. Hybrid fleets have become the practical default for operations of any meaningful complexity. The plant managers and procurement leads who actually run the numbers, who audit their duty cycles honestly, and who build strong supplier relationships on whatever fuel they end up running, are the ones whose operations will be most resilient over the next decade.

The forklift decision is not a one-time fleet purchase. It is an ongoing operational discipline. Treat it that way and the math will keep working in your favour.

Sources & Further Reading

US Energy Information Administration, Mont Belvieu Propane Spot Price data (2026). | First Energy Corporation, electric vs. propane forklift operating cost studies. | Propane Education & Research Council (PERC), forklift propane fleet data. | Mordor Intelligence, United States Backup Power Systems Market Report, 2026. | Argus Media, Global LPG Market Outlook, 2025-2026. | Material Handling Industry (MHI) Advanced Energy Council publications. | Industry data from Yale, Hyster, Toyota, Crown, and Mitsubishi Logisnext forklift programs.